AI Investment Trends 2026: Where Smart Money Is Going

Quick Summary

The 2025 AI shakeout separated hype from opportunity, giving serious investors a clearer map of where capital is concentrating in 2026. This analysis cuts throu

AI Investment Trends 2026: Where the Smart Money Is Actually Going

If you’ve been watching the AI space closely, 2025 felt like a shakeout year. The hype cooled just enough for serious investors to separate signal from noise — and what emerged is a clearer picture of where capital is concentrating heading into 2026.

Claude AI.svg" alt="anthropic logo" style="height:32px;width:auto;display:inline-block;margin:0 8px;filter:grayscale(50%) brightness(1.5);opacity:0.7;" title="">

Claude AI.svg" alt="anthropic logo" style="height:32px;width:auto;display:inline-block;margin:0 8px;filter:grayscale(50%) brightness(1.5);opacity:0.7;" title="">

This isn’t about moonshots or vague “AI everything” bets. The money moving right now is going into specific categories, specific use cases, and increasingly, specific workflows. Let’s break it down.

The Big Shift: From Models to Applications

For the past few years, the bulk of AI investment poured into foundation model companies — OpenAI, Anthropic, Mistral, Google DeepMind. That’s not stopping, but it’s slowing as a percentage of total AI spend. The new battleground is the application layer.

According to Sequoia Capital, the question investors are asking has changed from “which model wins?” to “which applications built on top of these models actually retain users and generate revenue?” That’s a fundamentally different investment thesis.

What this means practically: vertical AI tools — software built for a specific industry or workflow — are attracting serious Series A and B rounds right now. Think AI for legal contract review, AI for clinical documentation, AI for supply chain optimization. Not general chatbots. Specific, deep tools that replace or augment expensive professional labor.

Why Vertical AI Is Winning the Funding Race

General-purpose AI tools face a brutal commoditization problem. If you build a generic writing assistant, you’re competing with ChatGPT, Claude, Gemini, and a hundred other products — and you’re probably losing on price.

Vertical AI sidesteps this. A tool built specifically for radiologists reading MRI scans, or for accountants doing multi-entity reconciliation, has a defensible moat. The training data is specialized, the UX is purpose-built, and the switching cost for users is high once they’re embedded in the workflow.

Investors love that combination. Andreessen Horowitz’s AI-focused fund has been particularly vocal about this thesis, with multiple portfolio companies focused on AI for healthcare, legal, and financial services AI applications.

Agentic AI: The Category Attracting the Biggest Checks

If there’s one term that defined AI investment conversations in 2025, it’s “agentic AI.” And it’s not slowing down heading into 2026 — it’s accelerating.

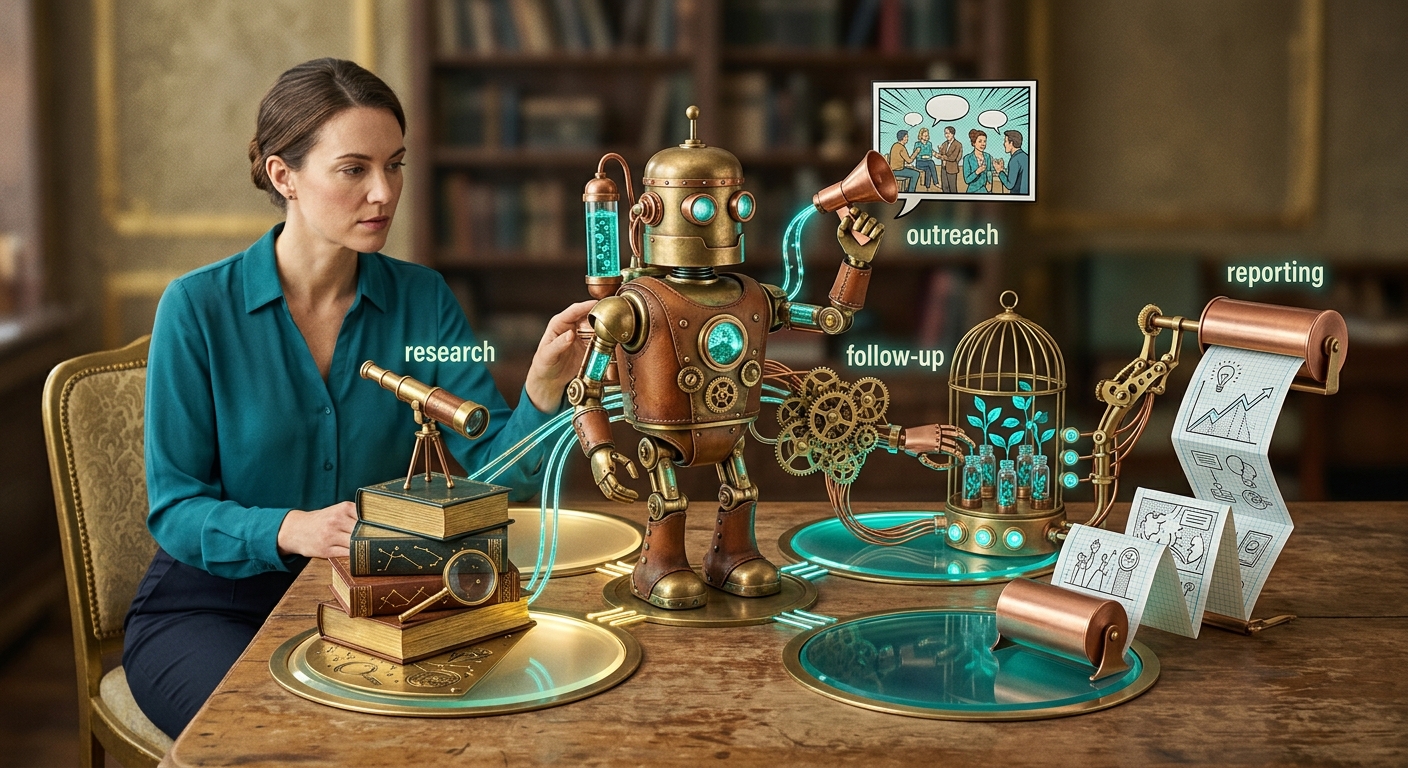

Agentic AI refers to systems that don’t just answer questions but actually complete multi-step tasks autonomously. Think of an AI that doesn’t just draft an email — it researches the recipient, finds the right contact information, sends the email, monitors for replies, and follows up automatically.

AI agent workflow with multiple connected steps: research, outreach, follow-up, and reporting — showing " title="">

AI agent workflow with multiple connected steps: research, outreach, follow-up, and reporting — showing " title="">Companies like Anthropic (with Claude’s computer use capabilities), Microsoft (with Copilot Agents), and Salesforce (with Agentforce) are all racing to own this category. The VC money is following them — and the startups building on top of these platforms.

Where Agentic AI Money Is Concentrating

Three specific agentic categories are pulling outsized investment right now:

- Sales and outbound automation: AI agents that prospect, personalize outreach, handle objections, and book meetings with minimal human input

- Customer support automation: Not basic chatbots, but agents that can actually resolve complex issues, access backend systems, and escalate intelligently

- Internal operations: AI that automates reporting, data reconciliation, compliance checks, and other back-office work that currently requires expensive human labor

At GSI, we’ve been building in the agentic space for over a year — our Operations Autopilot service is specifically designed to help businesses deploy this kind of automation without needing an internal AI engineering team. The demand has been consistent because the ROI is concrete and fast.

Infrastructure Bets: The Picks-and-Shovels Play

Beyond applications, infrastructure remains a massive investment category — though it’s getting more nuanced. The early infrastructure bet was simple: GPUs. Nvidia made that obvious.

The 2026 infrastructure thesis is more layered. Investors are now looking at:

Inference Optimization

Training models is expensive. Running them at scale is also expensive — and that’s where the unsolved problem lives. Companies like Groq, Together AI, and Cerebras are building chips and infrastructure specifically optimized for inference (running AI, not training it). This is attracting significant capital because every AI application company needs cheaper, faster inference to make their unit economics work.

Data Infrastructure and Vector Databases

AI applications are only as good as the data they can access. Vector databases — tools like Pinecone, Weaviate, and Chroma — allow AI systems to efficiently search and retrieve relevant information from massive datasets. This sounds technical, but it’s foundational: without good data infrastructure, agents hallucinate, retrieval fails, and applications break.

PitchBook data shows vector database companies saw a significant uptick in funding rounds through 2025, and that trend is continuing as more enterprise AI deployments require this infrastructure layer.

Observability and AI Ops

Once you deploy an AI system, how do you know it’s working correctly? How do you catch when it starts hallucinating or making errors? This is the AI observability problem, and it’s getting a lot of investment attention. Tools like Langsmith, Arize, and Weights & Biases are building the monitoring and debugging infrastructure that enterprise AI deployments need.

The Enterprise AI Budget Shift: What CFOs Are Actually Approving

Here’s a perspective that doesn’t get enough attention in investment trend coverage: where enterprise budgets are actually going, not just where VCs are betting.

Enterprise AI spending in 2025 shifted noticeably away from “AI strategy consulting” and toward actual implementation. Companies that spent two years doing AI readiness assessments are now being pushed by their boards to show ROI — which means buying tools that do things, not paying consultants to make presentations.

The categories getting approved fastest in enterprise budgets:

- AI-assisted sales tools: Gong, Clay, Apollo with AI features, and increasingly custom-built outbound systems

- Customer service automation: Intercom’s AI features, Zendesk AI, and specialized tools like Decagon and Sierra

- Content and marketing automation: Not just Jasper or Copy.ai — but integrated workflows that connect AI writing to publishing, SEO analysis, and distribution

- Internal productivity: Microsoft 365 Copilot is the big enterprise winner here, but specialized tools for finance, legal, and HR are growing fast

For businesses looking to move in this direction without building internal AI capability from scratch, our custom AI development service is specifically designed to deploy these kinds of systems fast, without the overhead of a full-scale tech buildout.

What’s Getting Defunded: The Contrarian View

Investment trends aren’t just about where money flows — they’re also about where it stops flowing. A few categories are cooling off as realistic expectations replace early-cycle enthusiasm.

Generic AI Wrappers

The “ChatGPT wrapper” business — taking an API call to OpenAI and building a thin UI around it — is essentially unfundable now unless you have extraordinary distribution or a very specific niche. The market figured out that there’s no moat in prompt engineering alone.

Consumer AI Apps Without Clear Monetization

The consumer AI app space burned a lot of investors who funded growth without figuring out willingness to pay. Character.ai, various AI companion apps, and general productivity tools all discovered that users love free AI and resist paying for it. Enterprise and prosumer markets are where the monetization is actually working.

Overly Broad “AI Platforms”

The “build anything with AI” platform pitch has largely failed to resonate with investors who’ve seen how difficult it is to win without a specific use case. No-code AI builders are finding it hard to differentiate, and the market is consolidating quickly.

The Geographic Dimension: Where Global AI Investment Is Concentrating

The US remains the dominant AI investment market, but the geographic spread is more interesting than the headline numbers suggest.

Europe is seeing significant investment in AI for regulated industries — healthcare, finance, and legal — largely because European companies are more cautious about deploying American AI tools that might conflict with GDPR and the EU AI Act. This is creating opportunities for EU-based AI startups with compliance-first positioning.

The Middle East is deploying AI investment at a sovereign fund level, with Saudi Arabia’s Public Investment Fund and UAE’s G42 making large bets on AI infrastructure. These aren’t just financial investments — they’re strategic bets on becoming AI hubs.

According to McKinsey’s State of AI research, the gap between AI leaders and laggards — both at the company and country level — is widening. The companies and economies investing now in serious AI capability are pulling ahead in ways that will be difficult to reverse.

Practical Takeaways: What This Means If You’re Not a VC

Investment trends matter to regular business owners and operators, not just fund managers. Here’s how to read what the smart money is doing and apply it to your own situation.

If you’re building a SaaS product: Vertical AI features are now a table-stakes expectation, not a differentiator. Niche deeper, not broader. The funding environment rewards specific expertise applied to specific problems.

If you’re running an existing business: The tools that are attracting the most enterprise spending — sales automation, customer support AI, internal operations automation — are available now at price points that make ROI calculations straightforward. The question isn’t whether to adopt them, it’s which ones fit your workflow.

If you’re evaluating AI vendors: Look for companies with real revenue, not just funding. The shakeout in the AI startup market means many funded companies won’t survive to 2027. Bet on tools with clear business models and sticky enterprise contracts.

If you’re thinking about where AI automation could work in your business: The agentic use cases — AI outbound sales, customer support, internal reporting — are the highest-ROI starting points that most businesses can deploy in weeks, not months.

The Bottom Line on AI Investment in 2026

The AI investment story in 2026 isn’t about picking the next model that beats GPT-5. It’s about finding the companies and workflows where AI automation creates durable economic value — lower labor costs, faster throughput, better customer outcomes — and investing there.

The shift from “AI is interesting” to “AI has to pay for itself” is actually healthy. It’s forcing real product discipline on startups, real ROI thinking from enterprise buyers, and real specificity from investors who got burned chasing hype in 2023 and 2024.

The businesses winning right now aren’t the ones with the most sophisticated AI — they’re the ones who identified two or three high-value workflows, deployed AI automation in those specific areas, and measured the results. That’s replicable. That’s where the real returns are, whether you’re an investor or an operator.

If you’re ready to figure out where AI automation actually makes sense for your business — not in theory, but in practice — reach out to the GSI team. We work with businesses at every stage to identify the highest-impact automation opportunities and build them fast.